Quant Bootcamp

6-day intensive training in Machine Learning for Quantitative Finance

ARPM builds advanced statistical competence to work in modern financial engineering, risk management and quantitative investment

Beyond-master online program: 5+5-month, multi-course, in-depth

Structured curriculum with live classes, support, and certification path

A complete, beyond master’s level curriculum that delivers unified understanding of Machine Learning and its applications to Financial Engineering, Risk Management and Quantitative Investment No gaps, no overlaps

One advanced curriculum, three complementary ways to learn

6-day intensive training in Machine Learning for Quantitative Finance

5+5-month, beyond-master program

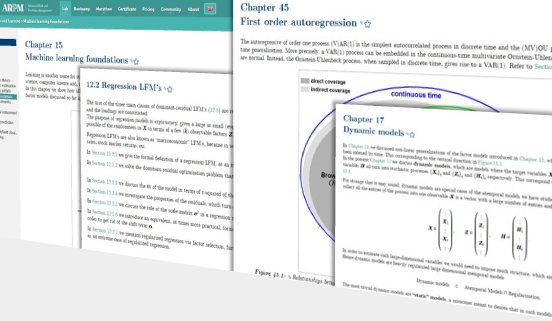

4,000-page e-textbook+AI tutor on Machine Learning for Quantitative Finance

Only ARPM has the Lab, a 4,000-page e-textbook on machine learning and its applications across all of quantitative finance, with code, animations, and an AI tutor, learn more.

Quant Bootcamp-ers and Certification holders, since 2009

All case studies and examples implemented on Jupyter Lab, no installation required

Overarching notation across Machine Learning and Quantitative Finance

These professionals chose ARPM for team upskilling. While company policy restricts official endorsements, they are happy to provide personal references upon request. All views expressed are their own and do not necessarily reflect those of their employers.